Price Performance Indicators

Previous Week | % Change | |

ICDX | $40.150 | -2,13% |

LME | $39.550 | 0,06% |

KLTM | $- | 0,00% |

SHFE | ¥279.690 | -1,69% |

USD/IDR | Rp14.343 | -0,24% |

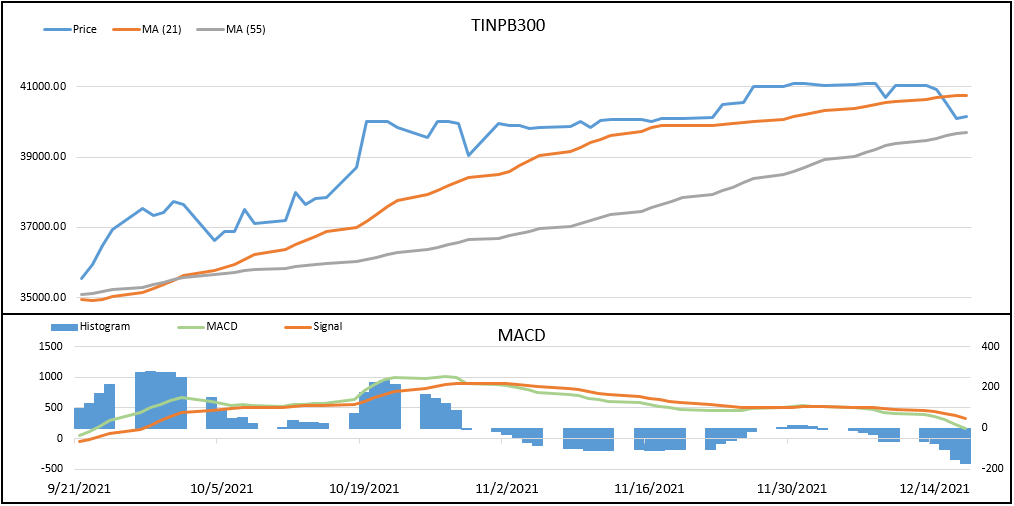

- In a week (13/12 - 17/12) the price of ICDX’s Tin dropped 2.13 percent.

- The highest volatility reached 0.82 percent.

Market Review

The average ICDX tin price throughout December until the third week was observed to move consolidated in the price range of USD 40,000 - 41,000 per tonne, weighed by the re-emergence of Covid-19 cases globally which prompted the re-imposition of tighter activity restrictions, causing tin price movements to get depressed.

The surge in Covid-19 cases, which are dominated by the Omicron, especially in Asia, back to threatens tin from the supply side, because around 70% of the global tin supply is supplied by Asia. Referring to the latest customs data released, China's imports of concentrate and tin ore in November reached 11,831 tons, down 40.35% compared to October. In addition, routine maintenance for about one month at the tin smelter Gejiu Kaimeng in Yunnan, which produces around 600 - 700 tons of refined tin, further strengthens the indications of a potential decline in tin output from China, the largest tin producer in the world.

Meanwhile, the demand side also showed a decline due to the re-imposition of activity restrictions to suppress the spread of the Omicron variant. Europe and the US are entering winter and coupled with a surge in the spread of Covid-19 caused industrial and manufacturing activities to have decreased in these tin-consuming countries.

Market View

Omicron Variant Soars, Will MSC Reimpose Force Majeure Status?

Since officially entering force majeure status on June 7, 2021, finally, Malaysia Smelting Corporation (MSC) has been active again on December 21. However, the rapid increase in Covid-19 cases in Asia caused by the Omicron variant, it has sparked concerns about the possibility of the re-implementation of force majeure. MSC accounted for around 330,000 tonnes or 7% of the total global supply last year, citing data from the International Tin Association (ITA). Thus, it is not surprising that the complete cessation of MSC activities since last June has contributed to the increase in global tin prices.

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

20-Dec | UK - CBI Industrial Order Expectations | 24 | 20 | 26 |

21-Dec | USA - CB Leading Index | 1.1% | 0.9% | 0.9% |

21-Dec | Uni Europa - Consumer Confidence |

| -8 | -7 |

22-Dec | China - CB Leading Index MoM |

| N/A | 0.3% |

22-Dec | USA - CB Consumer Confidence |

| 111.1 | 109.5 |

23-Dec | USA - Core Durable Goods Orders MoM |

| 0.6% | 0.5% |

24-Dec | Japan - National Core PPI YoY |

| 0.4% | 0.1% |

24-Dec | Japan - Housing Starts YoY |

| 7.4% | 10.4% |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish