Price Performance Indicators

Product | Previous Week | % Change |

ICDX | USD 43,615 | 0.50% |

LME | USD 44,195 | 2.18% |

KLTM | N/A | - |

SHFE | CNY 338,770 | 2.13% |

USD/IDR | IDR 14,344 | -0.22% |

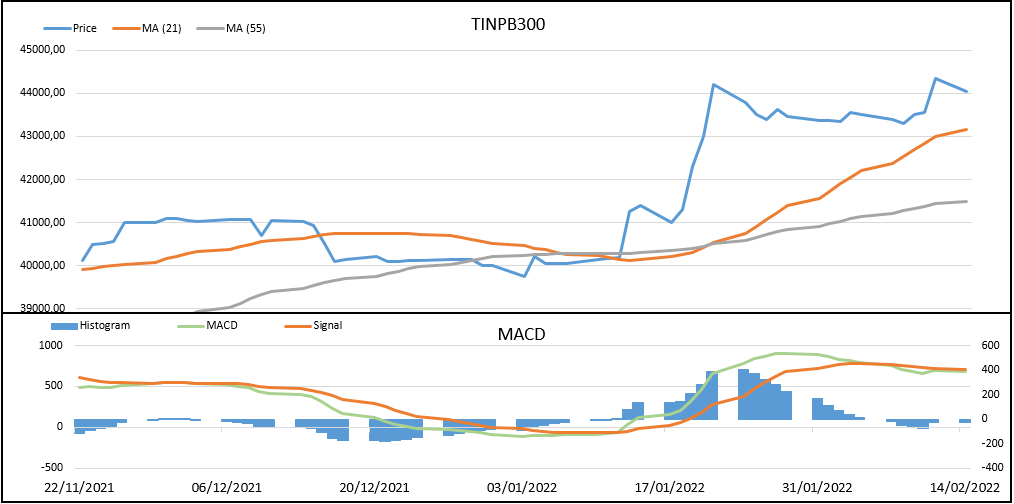

- In a week (7/2 - 11/2) the price of ICDX Tin slightly up 0.5 percent.

- The highest volatility reached 2.86 percent.

Market Review

Until the close of the second week of February, the price of tin was observed to be continuing its bullish trend, supported by tight supply and increasing demand from the global market after the recovery in global economic activity indicated by the lifting of lockdowns in various countries. The average price of ICDX tin in February reached a level above $43,000 per metric ton, an increase of almost 4% compared to the average price throughout January.

In Indonesia, so far 35% or 6 private tin exporters (ICDX's member) have obtained export quota in 2022, but until the second week of February, there were only 2 exporters who carried out export transactions. During January, the volume of tin export traded at ICDX reached 155.29 mt, decreased by 93.62% on a monthly basis, and decreased by 85.62% compared to the same period last year. At the same time, the continued increase in Covid-19 cases in the Bangka Belitung Islands Province has also become a market focus because it has the potential to encourage the imposition of restrictions on mining and smelting activities in the area which is the center of the tin producing in Indonesia.

Meanwhile, in China, which celebrated the Chinese New Year (CNY) holiday, factories have begun to close their factory activities since the last week of January and most of the smelters are expected to resume production after the Lantern Festival celebrations which fall on February 15. However, some smelters that were still operating during the CNY holiday were observed to have started to actively deliver tin into the SHFE warehouse, which quoted from the Shanghai Metal Market (SMM), the total stock on February 11 rose to 93,100 tons. In terms of production, SMM estimates that throughout February, China's refined tin production will decline to 11,540 Mt. As for the decline, it was influenced by a decrease in the supply of raw materials from Myanmar due to the surge in Covid cases and coupled with the problem of electricity costs in China which were still high due to rising coal prices.

Market View

High Electricity Costs, China Strive to Lower Coal Price Surge

Domestic coal prices in China are still at their highest level in 4 months. In an effort to dampen the surge and bring it down to levels below 900 yuan per mt - domestic coal prices are considered stable - the Chinese government has asked major coal producers to increase production early with a daily production target of 12 million mt. The increase in coal prices certainly contributed to an increase in the production costs of the smelter plant. For every 100 yuan per my increase in thermal coal price, electricity costs will increase by 520 yuan per mt, said the source quoted by Shanghai Metal Market (SMM). However, with the restrictions on Indonesia's coal exports and the potential increase in natural gas prices in Europe, will coal prices stabilize, or will they skyrocket?

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

15-Feb | USA - Empire State Manufacturing Index | 3.1 | 11.9 | -0.7 |

16-Feb | China - Consumer Price Index (CPI) YoY | 0.9% | 1.0% | 1.5% |

16-Feb | China - Producer Price Index (PPI) YoY | 9.1% | 9.5% | 10.3% |

16-Feb | Japan - Tertiary Industry Activity MoM |

| 0.3% | 0.4% |

16-Feb | Uni Europa - Industrial Production MoM |

| 0.4% | 2.3% |

16-Feb | USA - Industrial Production MoM |

| 0.4% | -0.1% |

17-Feb | Japan - Core Machinery Orders MoM |

| -2.0% | 3.4% |

17-Feb | USA - Philly Fed Manufacturing Index |

| 19.9 | 23.2 |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish