Price Performance Indicators

Previous Week | % Change | |

ICDX | $ 33,600 | 2.47% |

LME | $ 32,946 | -0.05% |

KLTM | $ 31,550 | 0.00% |

SHFE | ¥ 211,630.00 | 0.55% |

USD/IDR | Rp 14,539.01 | 0.64% |

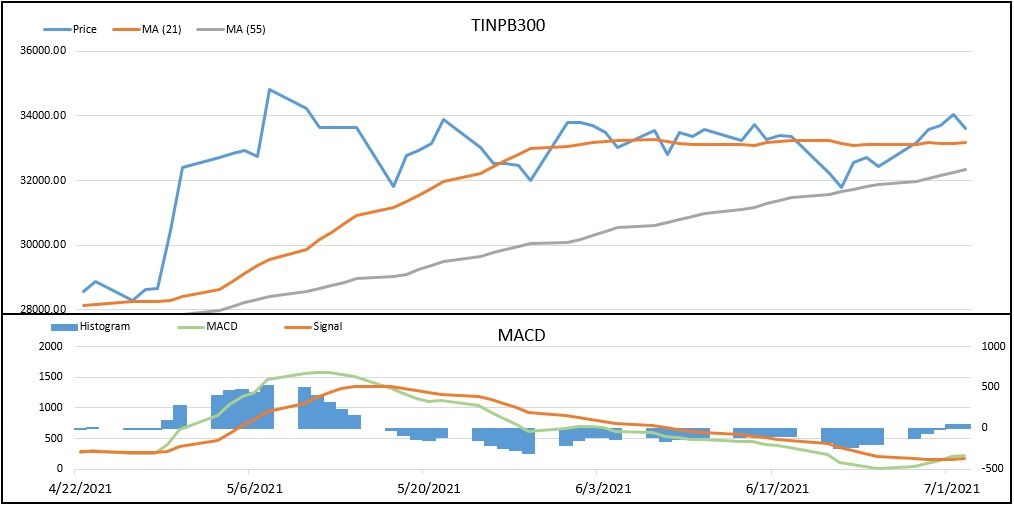

Market Review:

- In a week (28/6 - 2/7) the price of ICDX’s Tin edged up 2.47 percent.

- Price range between US$ 32,790 - US$ 34,050 per ton.

- Highest volatility reached 1.92 percent.

Entering July, the price of tin was observed to still move positively above $30,000 per tonne. Quoting transaction prices on ICDX, the average tin price during June was $33.825 per tonne, with the lowest price reaching $33,600 per tonne and the highest price reaching $34,050 per tonne. The re-emergence of new cases of the Covid-19 triggered by the Delta variant has the potential to threaten the demand side and disrupt the production, especially due to restrictions on activities at mining sites and tin smelters.

Quoted from the latest customs data, Myanmar, the main supplier of tin ore and concentrate to China, reported a significant decline in exports in May due to labor shortages in the country's main tin mining area. China imported about 11,159 tonnes of tin ore and concentrate in May, down about 42% or nearly 8,000 tonnes, of which more than half the weight of total gross imports came from Myanmar.

Meanwhile, China's largest smelter, Yunnan Tin, on June 24 had announced they would halt production at theirs main smelter in Yunnan province – which is one of the largest in the world – due to routine maintenance schedules that can take up to 45 days. The announcement provided support for the tin market, especially in China, which facing a supply issue.

Market View:

MSC Force Majeure Status Extended

Malaysia Smelting Corporation (MSC), the world's third largest refined tin producer, has extended force majeure status for shipments to customers. The status started on June 7 after the Malaysian government rejected MSC's application to be included in the list of essential service companies that can operate during the 3rd Movement Control Order (MCO 3.0). Malaysia started implementing FMCO 3.0 from June 1 and was scheduled to end on June 28, but citing an official statement from the Prime Minister of Malaysia, Tan Sri Muhyiddin Yassin on June 27 it was announced that the status would remain in effect as long as the number of cases in Malaysia remained high.

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

5/Jul | China - Caixin Services PMI | 50.3 | 54.8 | 55.1 |

7/Jul | Japan - Leading Indicators | - | 102.8% | 103.8% |

7/Jul | Uni Europa - German Industrial Production MoM | - | 0.5% | -1.0% |

7/Jul | USA - IBD/TIPP Economic Optimism | - | 57.3 | 56.4 |

8/Jul | Japan - Economy Watchers Sentiment | - | 41.9 | 38.1 |

8/Jul | China - New Loans | - | 1825B | 1500B |

9/Jul | China - CPI YoY | - | 1.3% | 1.3% |

9/Jul | China - PPI YoY | - | 8.8% | 9.0% |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish