Price Performance Indicators

Product | Previous Week | % Change |

CPOTR | Rp 15,570 | -7.29% |

FCPO | MY 5,269 | -1.78% |

Soybean Oil | $59.02 | -3.25% |

COFU | $67.79 | -2.64% |

USD/MYR | MY 4.2370 | -0.14% |

USD/IDR | Rp 14,280 | 0.90% |

CPOTR Focus:

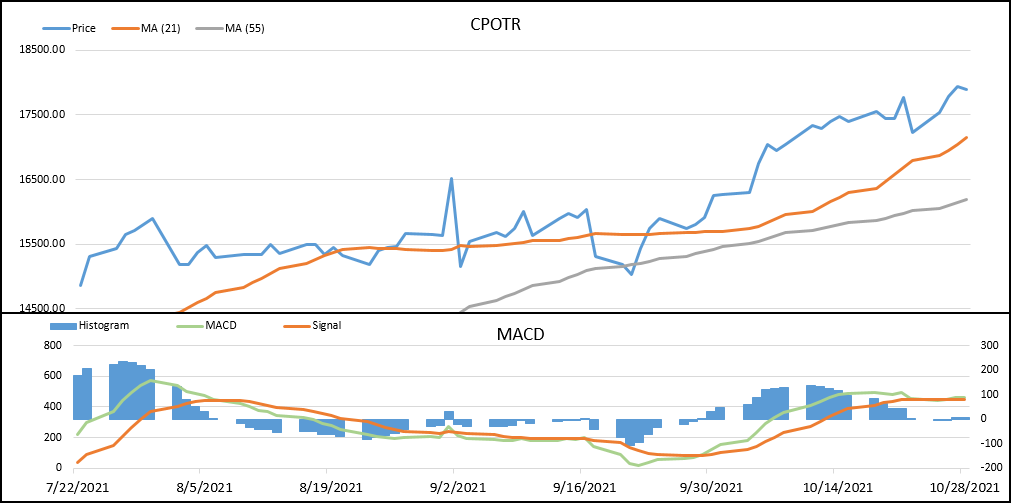

- (26/11 – 03/12) CPO price closed the week with a sharp correction of 7.29%

- The new variant of COVID-19 colors the market sentiment

During the week, crude palm oil (CPOTR) contracts were observed to be moving in a downward trend and closed the week with a significant correction of 7.29% - closing at Rp 15,1570,- per kg. The risk-off mood combined with bad sentiment around the crude oil market has been the main headwind for palm oil in the past week. However, market players still expect a corrective pullback ahead of the year-end season which usually boosts demand for CPO.

Crude oil prices has posted their steepest daily decline since April last year as the new COVID-19 variant spooked investors and added to concerns that the supply surplus could swell in the first quarter, ultimately making palm oil a less attractive choice for biodiesel feedstock. In fact, with crude oil always being one of the main indicators of global economic activity, some analysts still suggest the energy benchmark will remain weak as traders will take a cautious stance given the negative market developments.

Meanwhile, expectations for price recovery tend to be strong considering the end of the year season which usually increases people's activities towards food and beverage consumption – one of the main sectors that absorb the most palm oil products and their derivatives. However, with up-and-down developments related to the pandemic, namely the new variant of Omicron, the impact is still unclear. Going forward, further confirmations will still be eagerly awaited by the market. From the specifics of the industry itself, market participants suggest that future short-term price movement will be influenced by the November supply and demand forecast ahead of the actual data from the Malaysian Palm Oil Board (MPOB) on December 10, 2021.

Market View

New Variant, New Uncertainty

On 26 November 2021, WHO released the nickname for the sample variant B.1.1529 Omicron and classified it as a Variant of Concern (VOC) - and on 1 December 2021 the first confirmed case of Omicron was identified. As far as research is concerned, the Omicron variant is likely to spread more easily than the early SARS-CoV-2 virus and how easily Omicron spreads compared to Delta is still unknown. More data are needed to determine whether Omicron infection, and especially reinfection and breakthrough infection in fully vaccinated persons, causes more severe effects than other variant infections. Until now, vaccines are still expected to protect against more severe impacts. However, the question will always be; Will Omicron's sentiment continue to depress CPO prices due to the risk of low demand or will the pressure stop soon by welcoming positive developments?

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

7-Dec | CN – Improts NOV | - | 21.0% | 20.60% |

8-Dec | MY – Retail Sales YoY OCT | - | 5.3% | -1.1% |

8-Dec | EIA - Crude Oil Inventories | - | -1.5M | -0.9M |

9-Dec | CN – Inflation Rate YoY NOV | - | 2.6% | 1.5% |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish