Price Performance Indicators

Product | Previous Week | % Change |

CPOTR | Rp 15,540 | 0.58% |

FCPO | MY 4,550 | 0.53% |

Soybean Oil | $59.00 | -5.53% |

COFU | $68.79 | 0.44% |

USD/MYR | MY 4.1440 | -0.22% |

USD/IDR | Rp 14,261 | -0.25% |

CPOTR Focus:

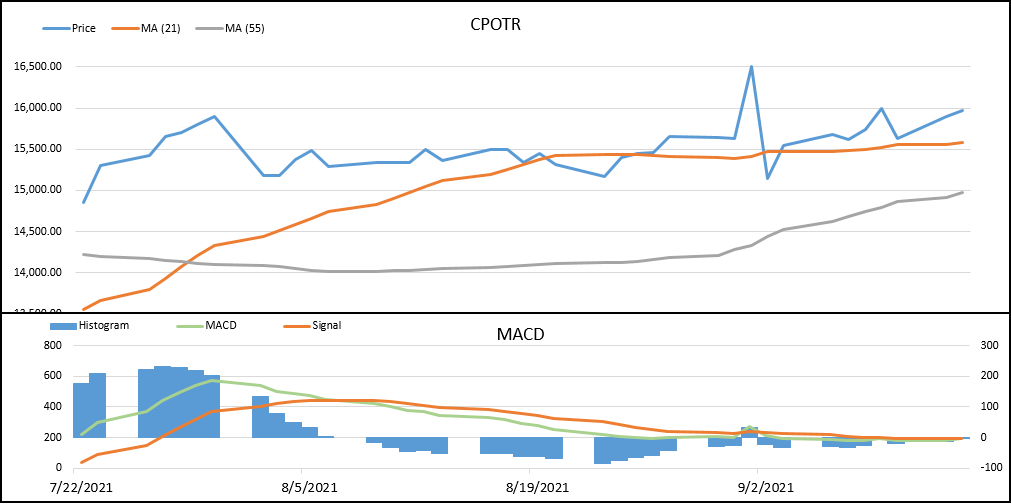

- 03/09 – 10/09) CPO prices closed the week with a slight gain of 0.58%

- There is a fear of oversupply in producing countries

After undergoing a fluctuating trend, finally the crude palm oil (CPOTR) contract ended last week with a slight weekly appreciation of 0.58% to the level of Rp 15,630, - per kg. In detail, after having strengthened for three days in a row, CPO then reversed to collapse in the last two days of the week. Sentiment related to the balance of supply and demand is still the latest focus of overall prices. Meanwhile, behind that, there is also a psychological factor in which a fairly sharp increase in CPO prices makes CPO prices vulnerable to correction.

The level of supply that is expected to increase from the two main producing countries, Indonesia and Malaysia, is a strong reason for the drop in CPO prices on the last day of last week. The Malaysian Palm Oil Board (MPOB) reported that CPO stocks at the end of August jumped 25% from the previous month to 1.87 million tonnes - the most in 14 months. In addition, MPOB also reported production levels rose 11.8% while exports slumped 17% - fueling oversupply concerns. Meanwhile, domestically, the Indonesian Palm Oil Association (GAPKI) reported that CPO production in July was still at a fast pace of 4.1 million tons, up 5.4% from last year, but down 9.5% from June.

On the other hand, exports reported by Malaysia actually fell by 17.06% in August 2021 from July 2021 to 1.16 million tons. However, a number of industry players also predict a recovery from the level of Malaysian CPO exports, at least in the early weeks of September – although no further confirmation has been received. One survey firm estimated that in the period 1st to 10th September, Malaysia's exports – mainly to China and India – would jump 57% to 572,345 tonnes from the same period in August of 364.546 tonnes.

Going forward, palm oil corrections will still be sensitive to the development of tightened social restrictions policies in two large producers, namely Indonesia and Malaysia to reduce the spread of COVID-19. Previously, cases of Covid-19 in Indonesia during the past month had shot up before sloping down in early September, prompting the government to ease the Restrictions on Community Activities (PPKM) – but at the same time, the addition of cases in Malaysia is actually at a high level.

Market View

Losing Export Potential by Indonesia’s B20-B50

Based on research from LPEM FEB UI, in 2020 until 2025 Indonesia may lose to thousand trillion of CPO export value. The thousand trillion lose may cause due to the implementation of B20 to B50 diesel fuel. With B50 implementation, the highest lose may reach around IDR 1.825 trillion. These condition may cause two potential result which are lowering Indonesia diesel import by the implementation of B50 or risk on losing Indonesia’s position in international CPO Market as lower CPO supply left to export. Will the B20 to B50 implementation giving Indonesia a more plus then minus to Indonesia industry and CPO market?

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

14-Sep | IN – WPI Food YoY AUG | - | - | 4.5% |

14-Sep | IN – Imports Final AUG | - | $47.01B | $46.4B |

15-Sep | CN – Retail Sales y/y | - | 12.30% | 12.10% |

15-Sep | US – Crude Oil Inventories | - | -3.6M | -1.5M |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish