Price Performance Indicator

Product | Previous Week | % Change |

COFR | Rp 1,037,000 | 0.83% |

COFU | $71.42 | 0.97% |

CPOTR | Rp 14,145 | 8.20% |

WTI | $71.81 | 0.36% |

BRENT | $73.59 | 0.69% |

USD/IDR | Rp 14,517 | -0.11% |

COFR Focus:

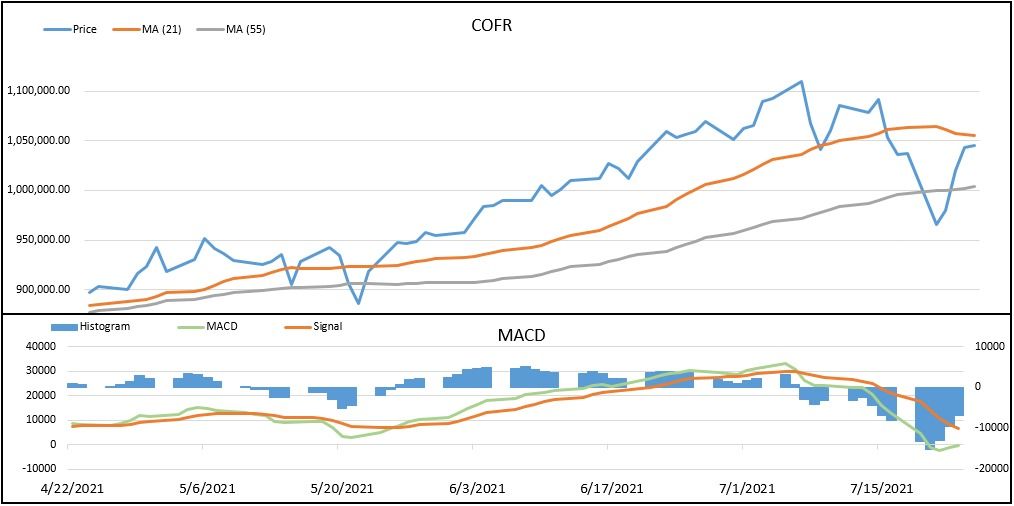

- (16/07 – 21/07) Crude oil appreciates slightly weekly at 0.83%

- COVID-19 is still the main driver of the energy sector

The COFR crude oil contract closed last week's fluctuations with a slight increase of 0.83% to Rp 1,045,600 per barrel. The narrow movement of crude oil last week occurred on the back of a tug of war of positive and negative sentiment absorbed by the market which is very sensitive to the stability of global oil supply and demand levels.

From the negative side, oil is still responding to a number of negative developments from the COVID-19 pandemic. Since last Friday, the market has been confronted with unfavorable news from various directions. From around Asia, OAG showed that scheduled flights in Asia experienced a drastic decline this week compared to the same week in pre-pandemic 2019, the decline was seen in Australia, Japan, South Korea and India, which fell 56.7%, 55.6%, 46.4% and 40.1% respectively, triggered by the earlier strong rebound in oil prices. The situation is exacerbated by the worsening Covid-19 daily data – urging a number of authorities from Australia, South Korea, and a number of Southeast Asian countries to re-implement activity restrictions.

Meanwhile, the increase in US crude oil inventories released by the API last week showed a significant increase in crude oil by 2.11 million barrels, far from what was previously predicted. This supply-side threat was also extended by the decision by OPEC and its allies to increase oil supply by 400,000 bpd from August to December 2021 in order to stabilize oil prices. In addition, OPEC+ also agreed to extend its production policy until the end of 2022 - from the initial agreement ending the deal in April 2022 - by setting new production allocations starting in May 2022.

On the positive side, and counterintuitive enough in some ways to cool sentiment, gasoline demand in many of the world's biggest oil consuming countries is seen by analysts as essentially returning to normal, judging by road traffic data showing the same trend. In addition, over the past two weeks, European aviation data shows European air traffic has approached two-thirds of flights in the same period in 2019.

Market View

Covid-19 Becomes the Main Focus, Oil Moves Cautiously

The threat of a decline in fuel demand from Asia as well as US statements regarding travel restrictions became negative catalysts that limited the movement of oil prices ahead. The US will not lift existing travel restrictions for now as cases of the Delta variant of Covid-19 are showing an increase in unvaccinated citizens and that increase is likely to continue in the next few weeks, the White House said in a statement released earlier in the week.

There is a potential for escalating US tensions with China

The US is considering cracking down on Iranian oil sales to China as it prepares for the possibility that Iran may not resume nuclear talks or may adopt a tougher line sometime under the leadership of Ebrahim Raisi, Iran's new president who will take office on August 5, a person said. US officials. The threat from the US has the potential to suppress Iranian oil sales because China is the largest importer of Iranian oil. However, on the other hand it also has the potential to heat up US relations with China, which could trigger new problems amid the current global economic recovery efforts.

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

28-Jul | EIA - Crude Oil Inventories | - | -2.6M | 2.1M |

29-Jul | US - FOMC Rate Statement | - | <0.25% | <0.25% |

29-Jul | US – Advance GDP q/q | - | 8.5% | 6.4% |

31-Jul | CN – Manufacturing PMI | - | 50.8 | 50.9 |

Riset Indonesia Commodity and Derivative Exchange

Crude Oil Weekly Newsletter

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish