BY LAMON RUTTEN

Understanding Backwardation and Contango in Commodity Market

Most commodity futures markets exhibit what can be described as a whiplash effect. At times, the price for a nearby futures contract is lower than that of further-away months, at other times, the nearby contracts trade at higher prices than the further-away months, and in yet other instances, the forward price curve has the shape of a lopsided smile. While the longer-term prices are relatively stable, prices for the nearby contracts can change fast, so the forward curve can change rapidly from backwardation to contango, and vice-versa.

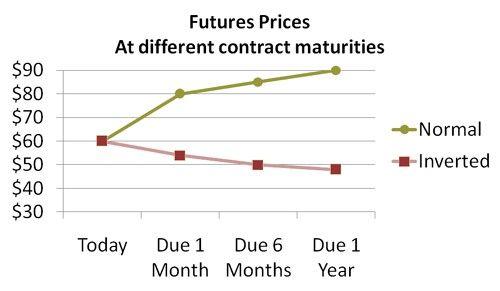

The graph illustrates a “normal” or “contango” forward price curve, and an “inverted” or “backwardated” curve. In particular in metal futures, markets are often in backwardation in the first contract month, and then the curve shifts to a contango, giving the shape of a smile.

Economists were for a long time baffled by backwardation. After all, the normal way for forward prices to behave is that prices for longer-dated commodity futures contracts should be higher than those for shorter-dated contracts. The price difference pays for the costs of storage; so in a normal market (they argued), the price for delivery in 3 months’ time should be equal to the price for delivery in 2 months’ time, plus one month of storage costs. Markets, of course, refused to behave according to these economists’ ideas.

Keynes' Theory on the Commodity Market

The first significant insight into why a market can be inverted comes from famous economist John Maynard Keynes, who in 1930 coined the term of “normal backwardation”. Keynes reasoned that the lower future price was necessary to pay a risk premium to investors/speculators. The physical markets are, by their nature, dominated by producers such as farmers, who are keen to reduce their price risk by selling futures contracts.

To incentivize speculators to buy futures contracts from them, the price of these contracts had to be below the expected future price of the commodities, so that speculators could expect to make a profit to compensate them for their risk. Thus, Keynes argued that what was called a “normal” price curve (contango) was in fact not normal at all, and that most markets at most times should normally be in backwardation.

Keynes, an avid speculator himself, was wrong in his explanation, as we now know, largely thanks to all the research that has been done to test Keynes’ Theory of Normal Backwardation. First, it is not true that in general, in futures markets the physical players tend to be dominated by sellers, and the speculative buyers tend to have net long positions.

Second, it is not true that futures prices are systematically lower than the actual future prices in physical markets. In fact, futures prices are good predictors of future physical prices. Third, it is not true that speculators are like insurers, taking on risk against the receipt of premiums; in fact, in liquid markets there is no risk premium at all that accrues to speculators (this is equivalent to an insurance market where one can get insurance for free… it seems too good to be true, but the balance of research shows that indeed, “insurance” on liquid commodity futures markets carries a close-to-zero cost. The reasons for that go beyond the scope of this blog).

When empirical tests of Keynes’ Theory of Normal Backwardation failed the theory, economists started looking for other explanations, and found them in the concept of convenience yield. If, say, a processor runs out of stock, he will be willing to pay a relatively high price for a fast delivery of the needed commodities. Thus, there is a premium for fast delivery and for holding commodities that are available for immediate delivery (as one can take delivery on futures contracts, nearby futures fall in this category).

Why would processors not keep enough stock to avoid being squeezed like this? Because storage has a cost, including in terms of working capital. Companies compare the two, and are willing to take a certain risk which, in many cases, will result on them bidding up the prices for immediate physical delivery – and thus, through arbitrage between the physical and futures markets, higher prices for nearby futures contracts.

With processing companies such as oil refineries or metal product producers moving to just-in-time delivery systems in the 1990s (reducing their stocks to as little as 1-2 weeks of normal usage), small disruptions in supply chains resulted in larger “shortage crises” among processors, forcing them into competitive bidding to secure the raw materials they needed.

The Impact of Investors' Behaviour in the Commodity Market

Commodity forward curves can also be affected by the behaviour of institutional investors, who tend to be long in further away contracts; and then “roll” their positions when they expire (in other words, they sell the now nearby futures contracts, and buy further-out contracts; if the market is in backwardation, they make an immediate profit). If a large investment fund does this, it can temporarily depress the prices of nearby contracts and inflate the prices of further-away ones.

And this brings us back to the whiplash. As the “convenience yield” of commodities is the highest in the near term (there is little convenience yield in holding stocks for the long term as there is more than enough time to procure the commodities in any of a number of ways), and the convenience yield is highly affected by short-term factors (like a strike at a mine, or an approaching hurricane that closes shipping routes), the value of the convenience yield fluctuates strongly.

In turn, this means that the value of nearby futures contracts can fluctuate strongly, even within a day. A commodity futures contract for the nearby March delivery may trade at a 5 US$/ton discount at 10 am, and at a 20 US$/ton premium at 12 am, just because of a new weather forecast. Meanwhile, the price of the May contract may hardly be affected by the news.

Market backwardations provide good opportunities for those holding excess stocks. If you are close to a futures market delivery point, and you have deliverable commodities that you do not immediately need, you can in effect make the market pay you for the right to store your commodities. What you do is to sell the nearby futures contract (say, March, trading at 100 US$/ton), and buy the next contract (say, May, trading at 90US$ a ton). You deliver against the March contract, thus encashing 100 US$/ton. And in May, you take the equivalent companies back, paying only 90 US$/ton.

Backwardation also looks interesting for speculators. They buy a contract; wait until it approaches delivery; then sell it, and buy a further-away contract at a lower price. Wait until that expires, and repeat…. Each time encashing the difference between the higher nearby-price and the lower further-away price.

Speculators should, however, be aware of the risks of this strategy – as noted, whiplashes happen and markets can rapidly move into a contango, forcing the speculator to roll at a loss or to (also expensive) take physical delivery and hold the stocks until they can be delivered back to the exchange…

The markets’ whiplashes provide interesting opportunities for arbitrage trading. The whiplash is, in fact, a temporary market abnormality, a distortion of the price relation between one contract month and the next. Because in the case of temporary disruptions, most trading activity tends to be in the nearest one or two contracts only, the further-away contracts can be “left behind” – but they will react in time, giving a profit to those who anticipated this delayed response.

Something similar applies to price relations across related commodities – e.g., there can be a whiplash in soya oil but not in palm oil, and a good speculator will know that the relationship between the two curves will eventually return to normal. For some commodities such as gold or silver, contango is the normal situation because there is so much stock compared to actual industrial use; but even here, the market can whiplash into backwardation, which a savvy speculator knows will not last.

In conclusion, for those investors/speculators who want to go beyond the simple “markets up, markets down” trading strategies, it will be interesting to look further into the themes of backwardation and contango, and see how they can apply their trading skills to the opportunities created by whiplashes along the forward price curve.

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish