Price Performance Indicators

Previous Week | % Change | |

ICDX | $36,680 | 3.24% |

LME | $37,525 | 7.99% |

KLTM | $31,550 | 0.00% |

SHFE | ¥279,500 | 8.51% |

USD/IDR | Rp14,256 | 0.16% |

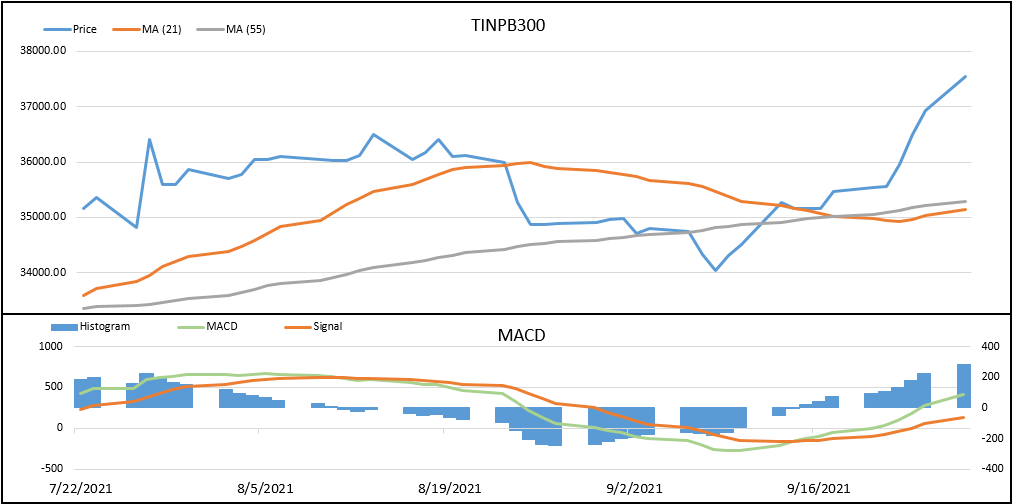

- In a week (20/9 - 24/9) the price of ICDX’s Tin rose over 3.24 percent.

- The highest volatility reached 0.62 percent.

Market Review

Towards the end of September, the ICDX tin price was observed to reach a new record, breaking a level above $37,000 per metric ton, or up nearly 60% compared to the tin price at the beginning of 2021. The decline in global tin stocks became the main catalyst that boosted the price increase.

The stock of tin in the LME exchange until the close of the fourth week of September was observed to fall 26% to a level of 1,155 tons compared to the final stock at the close of last August. In the KLTM market, it has been observed that it has not been operating since the closure due to the lockdown in June. The International Tin Association (ITA) projects that the potential deficit in the global tin market in 2022 will increase by 25% to 12,700 tons compared to 10,200 tons this year.

Meanwhile, the spike in Covid-19 infections in China forced the suspension of transportation at the China-Myanmar border, which resulted in a decrease in China's imports of tin ore and concentrates, Around 80% of China's tin ore and concentrates is coming from Myanmar. On the other hand, the output from mines in Myanmar has also fallen due to a shortage of labor, which has led to less than optimal production of tin mines in that tin major producing country. Imports from Myanmar fell by around 31% between July and August to around 3,100 tonnes.

Market View

Energy Crisis Forces China to Implement Electricity Rationing

China's efforts to keep power consumption under control and meet the demands of emission reduction policies have forced the government to issue strict regulations on energy consumption, which have an impact on reducing company operating hours and cutting production until halts of production. This year's warmer-than-average summer has led to a decline in energy supplies in China's southern provinces such as Yunnan, where about 30% of its electricity relies on hydropower. Meanwhile, soaring coal prices has also affected China's northern provinces, which rely on coal-fired power for their electricity. However, on the other hand, the energy crisis also contributed to a decline in demand from downstream tin industries such as solder, which had to reduce its production, and potentially offset the tin supply crisis in China's domestic market.

WEEKLY ECONOMIC DATA & EVENTS CALENDAR

Date | Data/Events | Actual | Expectation | Previous |

30-Sep | Japan - Prelim Industrial Production MoM |

| -05% | -15% |

30-Sep | China - Caixin Manufacturing PMI |

| 496 | 492 |

01-Oct | Japan - Tankan Manufacturing Index |

| 13 | 14 |

01-Oct | Japan - Final Manufacturing PMI |

| N/A | 512 |

01-Oct | Uni Europa - Final Manufacturing PMI |

| 587 | 587 |

01-Oct | UK - Final Manufacturing PMI |

| 563 | 563 |

01-Oct | USA - Final Manufacturing PMI |

| 606 | 605 |

01-Oct | USA - ISM Manufacturing PMI |

| 596 | 599 |

Source: ICDX Research

- EURUSD Bergerak Datar, Pasar Cermati Konflik Timur Tengah dan Prospek Kebijakan The Fed

- Minyak Menguat Dipicu Meluasnya Konflik AS - Iran ke Wilayah Regional Sekitar

- GBPUSD Melemah di Tengah Meningkatnya Permintaan Dolar AS sebagai Safe Haven

- Laju Bullish Minyak Bertahan Seiring Terus Berlanjutnya Serangan AS - Iran

- AS Kembali Blokade Pelabuhan Iran, Harga Minyak Ikut Melaju Bullish